"Doesn't TRICARE For Life cover Mom's memory care?"

That's the question many adult children ask when their military retiree parent starts showing signs of dementia or can't live independently. The assumption makes sense on paper. Dad served 24 years in the Navy. Mom has TRICARE For Life coverage as his widow. CHAMPVA was there for her sister. Surely one of these programs will handle the cost of memory care when the time comes.

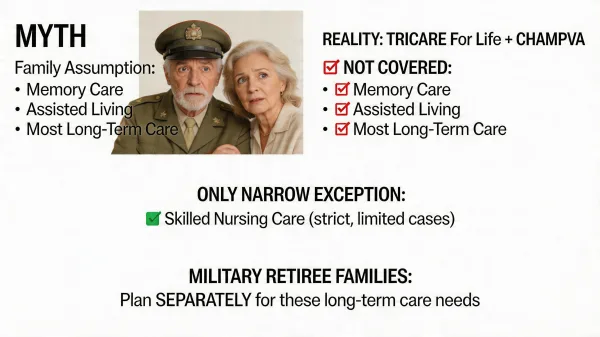

The answer is almost always no. TRICARE For Life long-term care coverage doesn't exist in the way most families assume, and CHAMPVA has the same gap. Both are Medicare-wraparound programs designed to cover medical care, not the daily supervision, custodial help, and residential support that memory care provides. The skilled-nursing exceptions that do exist are narrow, short, and tied to specific medical events.

This article walks through what TRICARE For Life and CHAMPVA actually cover for long-term care, where the coverage stops, the narrow places where they do help, and what military retiree families need to plan for separately. I've had to untangle these coverage rules three different times for family friends, and each time I came away realizing how widespread the misunderstanding is. If you've been counting on military health benefits to carry your parent through memory care or assisted living, the sooner you learn what they'll actually cover, the more time you have to build a real plan.

Does TRICARE For Life Cover Memory Care? The Short Answer

No. TRICARE For Life doesn't cover memory care, assisted living, or any form of custodial long-term care. CHAMPVA doesn't either. Both programs cover medical care, not the day-to-day supervision and help with daily activities that define memory care.

Both programs will pay for a narrow band of skilled nursing facility care when it follows a qualifying hospital stay, because they extend Medicare's skilled nursing benefit rather than replacing it. That's a short-term rehabilitation benefit, not a long-term care benefit. Once care shifts from skilled rehabilitation to custodial supervision (help with bathing, dressing, eating, and the cognitive supervision that memory care exists to provide), the coverage stops.

If your parent has early-stage dementia today and you're thinking five years ahead, neither TFL nor CHAMPVA will be paying the $7,000-plus monthly memory care bill.

What TRICARE For Life and CHAMPVA Actually Cover, and Don't

Understanding the gap starts with understanding what these programs are. TRICARE For Life is Medicare-wraparound coverage for military retirees and eligible family members once they enroll in Medicare Parts A and B. It pays the cost-sharing amounts Medicare leaves behind (deductibles, co-insurance, copays) for services Medicare covers. CHAMPVA works similarly for spouses, dependents, and survivors of veterans with a permanent and total service-connected disability. When a CHAMPVA beneficiary has Medicare, Medicare bills first and CHAMPVA picks up the remainder. The critical word in that description is "covers." Both programs piggyback on Medicare's coverage rules, and Medicare was never designed to pay for long-term care. Neither TFL nor CHAMPVA extends Medicare's coverage into new territory. Both fill gaps in Medicare's existing benefit structure, which is why the answer to "what does it cover" always routes back through "what does Medicare cover." The federal government's own guidance on TRICARE is direct: the program doesn't cover long-term care, nursing home custodial care, or assisted living facilities.

What these programs do cover

- Skilled nursing facility care after a qualifying hospital stay. Medicare covers up to 100 days of skilled care in a nursing facility if your parent had at least three consecutive inpatient hospital days (not counting discharge day) and entered the SNF within 30 days of discharge. TFL and CHAMPVA pick up Medicare's cost-sharing during that window.

- Home health care for skilled needs. Intermittent skilled nursing or therapy at home, ordered by a physician, is covered. Personal care and homemaker services are not.

- Hospice care. For a parent with a terminal diagnosis and a life expectancy of six months or less, hospice is covered through Medicare's hospice benefit, with TFL or CHAMPVA filling the cost-sharing gaps.

- Outpatient medical care related to dementia. Neurology visits, cognitive testing, medications through Part D, and related physician services are covered like any other medical condition.

- Inpatient mental health care. Limited inpatient psychiatric care is covered, which can matter for a parent in an acute crisis.

What they don't cover

Neither program pays for memory care, assisted living, adult day care, custodial nursing home care, or ongoing personal care at home. Supervising a parent with Alzheimer's, helping with bathing and dressing, medication management that isn't clinically skilled, and the residential component of any care setting all fall outside the benefit.

The skilled nursing benefit is the piece that confuses families the most. The benefit covers a stay that begins as rehabilitation, such as recovery from a hip fracture or a stroke, not a stay that begins as long-term placement. Once a patient no longer needs daily skilled care, the clock runs out. For a parent with dementia who needs daily supervision but no ongoing clinical care, that clock never starts.

From what I've seen working mobile X-ray in care facilities, the residents in skilled nursing beds on short-term rehab stays are a different population from the long-stay residents down the hall. Medicare pays for the rehab beds. Families pay for the long-stay beds. TFL and CHAMPVA don't change that math.

Where Military Retiree Families Get Hurt

The painful moment almost always arrives the same way. A parent has been managing on their own, or with spousal support, and then something shifts. A fall, a hospitalization, a new diagnosis, or the spouse's own decline. The adult children start pricing memory care and ask the financial question. That's when they learn the insurance card they've counted on for forty years doesn't apply to what they're actually facing.

Consider a retired Navy captain's widow with early-stage Alzheimer's. She assumed CHAMPVA and her husband's TRICARE For Life would cover memory care when she needed it, because that's what the family had always understood. Her adult children are now learning that neither will. They're trying to figure out what comes next, with less runway than they thought they had.

I've had to sit down with family friends three separate times and untangle these coverage rules, and every time the families were well-informed, had done their own reading, and still arrived at the same wrong conclusion. The coverage gap isn't hidden in fine print. It's a mismatch between how military families talk about their benefits and how those benefits actually work. What these programs promise is health care, not living care, and those aren't the same thing.

How Skilled Nursing Coverage Actually Works

For the narrow cases where TFL or CHAMPVA does help with facility-based care, the mechanics matter. Three consecutive inpatient hospital days (midnight to midnight) are required. Observation stays don't count, which trips up families whose parent was in the hospital for three nights but technically under observation status the whole time. Admission to a Medicare-certified skilled nursing facility must happen within 30 days of hospital discharge.

Medicare then pays the full cost for days 1 through 20. From day 21 through day 100, Medicare pays most of the cost but requires a daily co-insurance payment. TFL or CHAMPVA covers that co-insurance. After day 100, Medicare stops, and so does the primary benefit both programs rely on.

That's a 100-day ceiling on help from these benefits, and only if your parent qualifies for skilled care the whole time. The moment the facility determines your parent no longer needs daily skilled nursing or therapy, coverage ends. For dementia, which rarely triggers a qualifying hospital stay and rarely involves ongoing skilled care, this benefit almost never applies.

What Military Retiree Families Need to Plan For Instead

The real planning for long-term care sits outside the TFL and CHAMPVA benefit structure. Families who discover the coverage gap in their fifties have options. Families who discover it at seventy-five have fewer. The earlier the conversation starts, the more levers there are to pull.

Long-term care insurance

This is the purpose-built product for exactly this gap. Private long-term care insurance pays for memory care, assisted living, nursing home care, and home care, depending on the policy design. Premiums are meaningfully cheaper when bought in your late fifties or early sixties, and underwriting gets harder (and sometimes impossible) after a dementia diagnosis.

The Federal Long Term Care Insurance Program (FLTCIP) was historically available to federal employees, retirees, and many military personnel and their families. The U.S. Office of Personnel Management suspended new FLTCIP applications effective December 19, 2022, and the suspension remains in place as of 2025. Families shopping today are looking at commercial long-term care insurance or hybrid life/LTC policies.

VA benefits beyond TFL and CHAMPVA

The VA offers two long-term care pathways many military retiree families overlook. VA-enrolled veterans may qualify for care in VA nursing homes, Community Living Centers, State Veterans Homes, or contracted community nursing homes. Eligibility depends on the disability rating, income, and the specific service needed.

For wartime veterans and surviving spouses who meet income and asset limits, the VA pension program offers a cash benefit with an Aid and Attendance enhancement that helps pay for personal care. As of 2025, the maximum monthly Aid and Attendance benefit runs about $2,358 for a single veteran, $2,795 for a married veteran, and $1,515 for a surviving spouse. This is one of the few VA programs that directly helps with assisted living and memory care costs. Eligibility rules are strict and applications are slow.

Retirement-income replanning

When long-term care enters the picture, the income plan has to shift. Military retirement pay, Social Security, and any surviving spouse benefits become the base. The gap between that base and a $7,000 to $9,000 monthly memory care bill is where savings, home equity, long-term care insurance, VA benefits, and eventually Medicaid all come in. Few families can cover a decade of memory care from retirement income alone. Running that math five or ten years early changes everything.

VA Aid and Attendance: The Benefit Most Families Miss

Aid and Attendance is worth a closer look because it's the VA benefit most directly designed for the long-term care gap. It's an enhancement to the VA's wartime pension program, paid as tax-free monthly income to veterans or surviving spouses who need help with activities of daily living.

The service requirement is 90 days of active duty with at least one day during a wartime period, as defined by the VA. The medical requirement is documented need for help with daily activities (bathing, dressing, eating, mobility) or residence in a nursing home for mental or physical incapacity. The financial requirements are strict: the 2025-2026 net worth limit is $163,699, which combines assets plus countable annual income, with the primary residence excluded. A three-year look-back period reviews recent asset transfers, so moving money out of a parent's name late in the game can trigger a penalty that delays benefits. Unreimbursed medical expenses, including assisted living and memory care costs, can reduce countable income. That reduction is often what brings a family with retirement savings above the income cap into eligibility.

For a retired Navy captain's widow facing memory care costs, a $1,515 monthly Aid and Attendance benefit doesn't close the full gap. It does offset a significant share. Many widows of military retirees are eligible and don't know it, partly because the benefit sits quietly in a separate VA program, disconnected from the TFL world they've relied on for decades.

Medicaid: The Safety Net Few Military Families Want to Consider

For most middle-income military retiree families, Medicaid eventually enters the conversation. Medicaid is the largest payer of long-term care in the United States, and it covers memory care and nursing home care for people who qualify. The catch is that Medicaid is means-tested. Income and asset limits are strict, and the assets most families have worked a lifetime to build (the house, investments, retirement accounts) have to be spent down first.

Each state runs its own Medicaid program with its own rules, waiver programs, and look-back periods on asset transfers. Planning ahead, usually with an elder law attorney who knows the state's Medicaid rules, can protect some assets while preserving eligibility.

This isn't a path families choose first. It's the safety net after private resources, insurance, and VA benefits are exhausted. For families who plan early, the transition to Medicaid happens years later than it would otherwise.

How to Start Planning Today

If your parent is a military retiree or military widow, the planning work has three pieces. Pull their benefits statements and write down what's actually covered. Look at TRICARE For Life, CHAMPVA if eligible, any VA disability rating, and the pension situation. Know what you're working with before you look at care costs.

Next, price memory care and assisted living in your parent's market. Use the 2025 national medians as a floor: memory care around $7,500 per month and assisted living around $6,200, with significant regional variation. Run the annual math. That's the number the family planning has to meet.

Finally, talk to a VA-accredited claims agent or elder law attorney about Aid and Attendance eligibility, and if long-term care insurance is still a possibility, price a policy before a diagnosis makes it unavailable. These conversations are uncomfortable. They're also much easier at 65 than at 80.

The Bottom Line for Military Retiree Families

The gap between what military retiree families think their benefits will cover and what those benefits actually cover is one of the hardest truths in senior care planning. It's not because TRICARE For Life and CHAMPVA are bad programs. They do what they were designed to do, which is cover medical care for a population that earned it through service. Long-term custodial care was never in the design.

If you're reading this because a parent's situation is already shifting, the path forward is concrete. Learn exactly what's covered. Price the real care costs. Look hard at Aid and Attendance if there's any chance of eligibility. Bring in professional help on VA benefits and, where it's still possible, on long-term care insurance. These aren't abstractions. They're the decisions that determine whether a family runs out of money in year three or year eight.

The families I've helped with this each wished they'd started earlier. None of them wished they'd waited.