This article is for informational purposes only and does not constitute legal, financial, tax, or benefits advice. VA and Medicaid rules change frequently, vary significantly by state, and apply differently to each family's situation. Consult a VA-accredited elder law attorney or certified Medicaid planner before making decisions about benefits applications, asset transfers, or care placements. Do not rely on this article as a substitute for personalized professional guidance.

Can my parent receive VA Aid and Attendance and Medicaid at the same time? Yes, in most cases. A wartime veteran or surviving spouse can receive both A&A and Medicaid benefits concurrently, but the way the two programs interact depends heavily on the care setting, whether Medicaid is paying for a nursing home or for services through an HCBS waiver, and the state where your parent lives.

For families paying for memory care, this matters a lot. The combined benefits can cover a significant portion of monthly costs when your parent's care is provided through an assisted living or memory care community with an HCBS waiver attached. The rules shift if your parent ever moves to a Medicaid-covered nursing home, where A&A drops to $90 per month. And the rules governing when the two programs stack and when one reduces the other have changed significantly since 2018, when the VA added a three-year look-back period. For veteran families, getting the sequence right matters as much as getting the paperwork right. Filing one application before the other, or making a well-intentioned gift to a grandchild at the wrong time, can cost months or years of benefits that were otherwise yours.

I've seen what happens when a family burns through savings because they didn't understand how these benefits actually work together. The rules aren't obvious, and the strategies that worked a decade ago don't all apply now. The VA overhauled its pension rules in October 2018. What protects benefits in one program can disqualify them in the other. This article walks through how A&A and Medicaid actually interact in 2026, the look-back periods to plan around, the mistakes that cost families real money, and when you need an elder law attorney.

Understanding VA Aid and Attendance in 2026

Aid and Attendance is an enhanced VA pension for wartime veterans and surviving spouses who need help with daily activities or have a documented cognitive impairment requiring supervision. It isn't the same as VA disability compensation. A&A is needs-based, which means the VA looks at income, net worth, and unreimbursed medical expenses when deciding eligibility.

The 2026 maximum monthly amounts (Dec. 1, 2025 through Nov. 30, 2026) are approximately $2,358 for a single veteran, $2,795 for a veteran with a dependent, and $1,515 for a surviving spouse. The net worth limit for this benefit period is $163,699, which includes most assets owned by the applicant and spouse but excludes the primary home and one vehicle. What your parent actually receives each month depends on countable income and documented medical expenses.

Memory care qualifies as a medical expense for A&A purposes when the resident has a doctor's statement confirming they need help with activities of daily living or have a cognitive condition requiring supervision. For most families paying $6,000 to $9,000 a month for memory care, those expenses wipe out countable income and push the A&A payment close to the maximum.

How Medicaid Pays for Memory Care

Medicaid is the primary long-term care payer in the United States, but it doesn't pay for memory care the way families often assume. Traditional Medicaid covers nursing home care for people who meet income and asset limits, not assisted living or memory care communities. Memory care sits in a different category because it's considered residential care, not skilled nursing.

The path to Medicaid coverage for memory care in most states runs through a Home and Community Based Services (HCBS) waiver. These waivers let states pay for care services, including personal care, supervision, and help with daily activities, inside an assisted living or memory care community. The catch: Medicaid doesn't pay for room and board outside a nursing home. Families still cover that portion from Social Security, pensions, A&A, or other resources.

Each state runs its own HCBS waiver program with different names, services, income limits, and waitlists. Some waitlists run months. Others run years. Applying early, before your parent needs full-time memory care, can protect their spot.

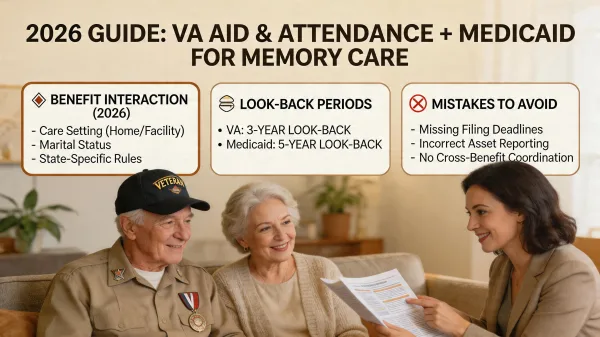

How A&A and Medicaid Actually Interact in 2026

The interaction between A&A and Medicaid depends on three things: which Medicaid program your parent is in, whether they have a spouse or dependent, and the state. The general rule is that your parent can receive both benefits, but the VA may reduce the pension once Medicaid starts paying for care.

When A&A and Medicaid Can Be Combined

If your parent is receiving memory care through a Medicaid HCBS waiver while paying for room and board out of pocket, A&A generally continues at full amount. The VA doesn't treat HCBS waiver services the same way it treats Medicaid-funded nursing home care. The A&A portion of the pension doesn't count against Medicaid's income limit in most states, which means the two benefits stack: A&A pays toward room and board, while Medicaid covers the care services.

This is the arrangement most memory care families are working toward. It keeps your parent in a familiar setting, protects more of the household's remaining assets, and preserves the full VA pension.

When Medicaid Reduces or Replaces A&A

If your parent moves into a Medicaid-funded nursing home and has no spouse or dependent child, A&A drops to $90 per month. That $90 becomes their personal needs allowance for small personal expenses inside the facility. The full pension doesn't disappear, but it stops functioning as a meaningful income source for the household. This reduction catches many families off guard when memory care progresses to a nursing home level of care.

If your parent has a spouse living in the community, the rules change. The pension doesn't automatically reduce to $90, because the community spouse needs income to maintain the household. Spousal impoverishment protections come into play, and the calculations get complicated fast.

State-by-State Variation

States handle the stacking differently. Some count only the basic pension portion against Medicaid's income limit and exempt the A&A enhancement. Others apply a different formula. A few have Personal Needs Allowance policies that let veterans keep some or all of the $90 reduction. This variation is why cookie-cutter advice doesn't work. Your parent's specific state rules control what the combined benefit looks like.

I watched a family member's dementia journey up close, and the financial piece caught us completely off guard. The monthly cost of memory care was double what the family had planned for, and the decline moved faster than anyone expected. What I learned from that experience, and what I've confirmed in researching this article, is that families who sit down and map out the A&A-to-Medicaid transition early end up in a far better position than families who wait until savings are running out. The math of combining benefits is workable when there's still runway. The problem is that the window for making smart moves closes fast once a crisis hits. By the time memory care bills are arriving and the Medicaid application feels urgent, many of the planning options have expired look-back windows, locked assets, or simply aren't available anymore. Starting two or three years early turns a painful transition into a manageable one.

Look-Back Periods You Need to Understand

Both the VA and Medicaid review asset transfers going back several years before an application. Gifts, below-market sales, and transfers to family members inside these windows can trigger penalty periods that block benefits at the worst possible time. The two look-backs don't match, which is where families run into trouble.

The Three-Year VA Look-Back

The VA added a 36-month look-back to pension benefits on October 18, 2018. Any asset transfer for less than fair market value during the three years before an A&A application can create a penalty of up to five years. The penalty is calculated by dividing the transferred amount by the MAPR for a single veteran ($28,296 in 2026). During the penalty period, your parent can't receive a VA pension or A&A.

Transfers made before October 18, 2018 are exempt, regardless of when your parent applies. Transfers to a spouse are exempt. Transfers that can be returned in full may eliminate the penalty. Transfers into certain trusts or annuities follow their own complicated rules and shouldn't be attempted without specific advice.

The Five-Year Medicaid Look-Back

Medicaid reviews 60 months of financial history before a long-term care application in 49 states and the District of Columbia. California uses a different rule, with a 30-month look-back for nursing home Medi-Cal that applies only to nursing home services. The penalty for a disqualifying transfer is calculated using the state's penalty divisor, the average monthly cost of nursing home care in that state. A $50,000 gift in a state with a $10,000 monthly divisor creates a 5-month penalty period.

The IRS annual gift exclusion of $19,000 per recipient in 2026 gives no protection against Medicaid's look-back. That's one of the most common points of confusion. A grandparent writing $15,000 checks to grandchildren for college over five years has gifted $75,000 from Medicaid's perspective, and that money triggers a penalty no matter how legitimate the gifting felt.

Why the Two Look-Backs Don't Line Up

A transfer made 40 months before an application sits outside the VA's three-year window but well inside Medicaid's five-year window. A family timing gifts around one program can create a penalty under the other. Dementia progresses faster than most families plan for, which shortens the window further. By the time a parent needs memory care, waiting out a five-year look-back isn't always an option. The earlier a family maps out both look-backs together, the more flexibility they keep.

Where Families Get Hurt: Planning Mistakes That Cost Benefits

A few specific mistakes show up again and again with families combining VA benefits and Medicaid. Most come from acting on generic advice or waiting too long to get specific help.

Gifting assets during the look-back. Adult children receiving $10,000 to $20,000 gifts, grandchildren receiving college checks, or a parent adding a child's name to a bank account all count as transfers. The VA and Medicaid both treat these as uncompensated unless they fit a narrow exception.

Applying for Medicaid before A&A. If your parent qualifies for A&A, Medicaid requires them to apply. Filing the Medicaid application first can delay the A&A determination and cost months of benefits.

Using the wrong kind of trust. Revocable living trusts offer no protection against either look-back. Irrevocable Medicaid Asset Protection Trusts work, but only if funded more than five years before the Medicaid application.

Paying family caregivers informally. Cash payments to an adult child who provides care look like gifts during a Medicaid review. A properly drafted personal care agreement with documented hours and fair market rates turns those payments into legitimate expenses.

From years doing mobile X-ray work inside assisted living and memory care facilities, I've seen firsthand how quickly a family's financial picture shifts once a parent is settled into care. The time to plan is before the move-in date, not after.

When to Call an Elder Law Attorney

An elder law attorney with VA accreditation and Medicaid planning experience isn't a luxury in most memory care situations. One consultation usually costs less than a single missed planning window. Call one when any of these apply:

Your parent has more than $50,000 in countable assets beyond a home and vehicle. The Medicaid asset limit is typically $2,000. Getting from one number to the other without triggering a penalty requires specific planning.

Your parent is a veteran or surviving spouse who might qualify for A&A. The VA application rewards documentation and punishes sloppiness. A VA-accredited attorney can file on your parent's behalf.

A spouse will stay in the community while the other enters memory care. Spousal impoverishment rules are unforgiving, and the CSRA in 2026 lets the community spouse keep up to $162,660 in most states.

You're 12 to 18 months out from needing Medicaid. That's still enough runway to put a plan in place. Inside that window, the options narrow every month. The National Academy of Elder Law Attorneys (NAELA) maintains a searchable directory by state.

A Realistic Family Transition Scenario

Imagine your father has lived in a memory care community for three years. His monthly cost is $7,800, covered through his pension, Social Security, and A&A of about $2,358. His remaining savings will run out in about 18 months. Your mother passed away two years ago, so there's no community spouse to plan around.

The family wants to transition to Medicaid without losing A&A or triggering a look-back penalty. Several moves need to happen in sequence. First, map out his state's HCBS waiver program for memory care, including the waitlist. Second, confirm no gifts or below-market transfers have happened in the last five years. Third, work with an elder law attorney to spend down remaining assets on exempt items like memory care bills, home repairs, or prepaid funeral arrangements.

If the HCBS waiver activates before savings run out, the transition works. A&A stays intact because he isn't in a nursing home. Medicaid covers the care services. The family covers room and board from his pension, Social Security, and A&A. The math gets tight, but it works.

Common Questions Families Ask

Can my parent apply for A&A and Medicaid at the same time? Yes, but the sequence matters. File the A&A application first if your parent qualifies, then pursue Medicaid. Medicaid requires applicants to apply for any benefits they're entitled to, which includes VA pension.

Will the $90 reduction apply in a memory care community? Usually no. The $90 reduction is specifically for veterans with no spouse or dependent in a Medicaid-funded nursing home. Memory care paid through an HCBS waiver is a different setting under the rules.

Do A&A payments count against Medicaid's income limit? In most states, the A&A portion of the pension is excluded from Medicaid's income calculation. The basic pension portion may count, depending on the state.

If I'm a caregiving adult child, can I be paid? Yes, but only with a written personal care agreement signed before the care begins, with hours documented and payments at fair market rates. Informal payments look like gifts during a Medicaid review.

What if my parent lives in California? California's rules are different. Medi-Cal has a shorter look-back for nursing home coverage and no look-back for the Assisted Living Waiver. The state has also been phasing asset limits in and out, so check current rules before making any planning moves.

Planning Starts Earlier Than You Think

Combining VA A&A and Medicaid for memory care can work, and for many families, it's the difference between keeping a parent in a familiar setting and running out of money. The benefits stack when they're set up correctly. The stacking breaks down when families gift assets inside a look-back window, apply in the wrong order, or assume the rules that worked for a neighbor will work for their family.

The biggest lesson from every case I've seen up close is that planning has to start earlier than families think. The moment a memory care diagnosis enters the picture, the planning clock is running. Five years of look-back is a long window, and dementia doesn't wait for it to close.

If your parent is a wartime veteran or surviving spouse, start the A&A paperwork now, even if you don't need it yet. Find a VA-accredited elder law attorney in your state. Walk through the look-back periods together. You don't have to figure this out alone, and you don't have to get it right on the first try. You just have to start.