As of April 2026, picture this: your 72-year-old mother was diagnosed with Alzheimer's last week. You're suddenly trying to understand what original Medicare actually pays for, whether her supplemental coverage is the right kind, whether she might qualify for a Medicaid waiver, and how to evaluate care options without losing your own job. Every search result leads to a different answer, and half of them want your phone number before they'll tell you anything useful.

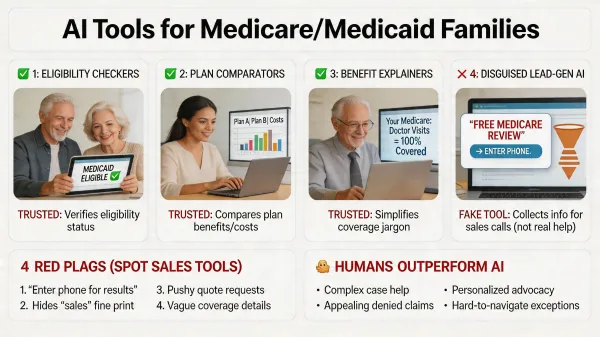

Three categories of AI tools help families with Medicare and Medicaid navigation: plan comparison tools with real explainability (the CMS Medicare Plan Finder is the trustworthy baseline), benefits eligibility screeners (the National Council on Aging's BenefitsCheckUp is the standard reference), and claims and denial analysis tools. A fourth category looks like the others but isn't, and it's the one that wastes the most family time. It's lead-generation marketing dressed up as a benefits navigator.

When my family went through a relative's dementia, we learned how much time gets lost trying to figure out Medicare, Medicaid, and secondary insurance while you're also grieving. The overwhelm is real. AI tools can help, but you need to know which ones are actually working for you and which ones are routing you to whoever paid them.

The Three Categories of AI Tools That Actually Help

Not every tool that calls itself an AI Medicare navigator is doing real work. The legitimate ones share something in common: they let you input specifics about your parent's situation and they show you how the answer was constructed. After almost twenty years working in hospitals, I can tell you the families who handle Medicare decisions best are the ones who use tools that show their work, because those are the only tools you can actually verify against reality.

Plan Comparison Tools with Real Explainability

The Medicare Plan Finder at Medicare.gov is the trustworthy baseline for comparing Medicare Advantage and Part D plans. You enter your parent's medication list with exact dosages, the providers they want to keep seeing, and their healthcare usage patterns, and the tool shows total annual cost across every plan available in their ZIP code, including premiums, deductibles, copays, and drug costs. Some third-party tools layer AI-powered natural language query on top, letting you ask questions like "which plan keeps my mom's neurologist in network and covers her donepezil with the lowest out-of-pocket cost?" For families just starting to understand what Medicare covers for memory care, that natural language layer is useful early on. The good AI tools explain why a plan ranked highest, and if a tool recommends a plan but won't show you the calculation, you're using a marketing wrapper.

Benefits Eligibility Screeners

The National Council on Aging's BenefitsCheckUp is the deepest reference here. You enter your parent's state, age, income, assets, household size, and health conditions, and the tool screens against more than 2,000 federal, state, and local benefit programs, surfacing what your parent likely qualifies for, including Medicare Savings Programs, Medicaid Home and Community-Based Services waivers, SNAP, LIHEAP, and state-specific senior support programs. Some state agencies have begun deploying AI chatbot front-ends on their Medicaid eligibility pages, and these are useful for general orientation, not for definitive eligibility determinations. Final Medicaid eligibility runs through your state's Medicaid agency and usually requires a formal application reviewed by a caseworker.

Claims and Denial Analysis

The third category is newer and increasingly useful. Several AI tools now let you upload a Medicare or Medicaid denial letter and they'll explain what the denial reason code means, what your appeal grounds are, and what the typical reversal rate is for that denial type. They'll often draft an appeal letter using language Medicare's appeal reviewers respond to. This is a meaningful capability, because Medicare denials reverse on appeal at surprisingly high rates when the appeal is filed correctly and on time. The catch is that medical necessity disputes (the hardest denials to overturn) usually need a physician's clinical statement and a benefits specialist who knows the appeal process. AI can scaffold the appeal, but it can't replace the clinical and procedural expertise that wins the contested cases.

How to Spot the Sales-Funnel Tools

Now the part that matters more than the recommendations: how to spot the lead-generation tools that look like benefits navigators but are marketing funnels for specific carriers. Four red flags surface within the first thirty seconds, worth knowing before you input anything sensitive about your parent.

Red Flag One: Contact Info Before Results

A legitimate tool shows you results first; a sales funnel asks for your phone number, email, or your parent's Medicare number before showing you anything useful. Medicare.gov and BenefitsCheckUp ask only for the information they need to run the screening, and they don't gate results behind a contact form. If a free Medicare AI tool won't show results until you've filled in your phone number, that phone number is the product.

Red Flag Two: Results Skew to a Narrow Carrier Set

When a tool consistently recommends plans from the same two or three carriers regardless of how you change inputs, you're looking at paid placement. Real plan comparison surfaces every plan available in a ZIP code and lets the math sort them. If you change your parent's medication list dramatically and the recommended plan barely moves, the tool isn't doing comparison work. It's selling lead routing.

Red Flag Three: Corporate Parent Is a Broker or Lead-Gen Company

Check the footer or About page. If the corporate parent is an insurance brokerage, a Medicare lead-generation company, or a marketing agency, the tool is built to generate leads, not give neutral guidance. Licensed independent brokers can be excellent advisors. The problem isn't brokers existing, it's a tool presenting itself as neutral while functioning as a captive sales channel for one carrier or a small set of paid partners.

Red Flag Four: Results Don't Reflect Real Medicare Rules

Toggle between income levels that should change Medicare Savings Program eligibility, and if the recommendations don't shift, the rules engine is fake. Real benefits tools reflect real rules. When the underlying logic isn't there, you're looking at marketing software, not a benefits navigator.

During my family's experience with a relative's dementia, we made the mistake of using one of these tools early on, the kind promising to find the best Medicare Advantage plan in five minutes. Within an hour, three agents from the same brokerage were calling, each pushing a slightly different version of the same plan, and none of them asked the actual important question, which was whether the neurologist managing her care was in network. We figured that out ourselves later, after she'd already enrolled. I've worked nearly twenty years inside hospitals, and the gap between what these tools tell families and what matters at the point of care is one of the most frustrating things I've seen.

The Specific AI Tools Worth Using as of 2026

As of April 2026, four specific tools and tool categories meet the standards above and consistently help families without routing them into sales funnels.

Medicare.gov Plan Finder

The CMS Medicare Plan Finder is the government-run baseline for comparing Medicare Advantage and Part D plans. It's free, neutral, and updated annually with official plan data. CMS has been piloting AI-powered enhancements that let users ask plan questions in natural language and get explanations of why one plan ranks higher than another. These pilots aren't fully deployed nationwide as of spring 2026, but they're worth checking when you start your research.

NCOA BenefitsCheckUp

The National Council on Aging's BenefitsCheckUp screens your parent against more than 2,000 federal, state, and local programs based on state, income, assets, and conditions. The interface has been refined repeatedly over the years and is the deepest starting point for benefits beyond Medicare. NCOA is a national nonprofit, and the tool's purpose is screening, not selling, which makes it the cleanest non-government starting point for caregivers building a benefits picture.

State-Level SHIP Programs

Every state has a State Health Insurance Assistance Program (SHIP), which provides free, unbiased Medicare counseling. Counselors are trained volunteers and staff who don't sell anything. Some state SHIP programs have begun deploying AI chatbots to handle initial questions before connecting families to a human counselor. The chatbots are uneven, but the human counselors remain valuable, especially for tricky cases. I've seen plenty of families come into the ER with the wrong Medicare Advantage plan for their situation, almost always because they used a tool that ranked plans by something other than the actual math.

ChatGPT, Claude, and General-Purpose AI for Research

For understanding terminology, summarizing benefit explanations, drafting questions to ask a SHIP counselor, or working through a denial letter, general-purpose AI assistants are useful scaffolding tools, though they aren't authoritative on rule specifics. Treat them like a knowledgeable friend who reads quickly: helpful for orientation, valuable for prep work, but always cross-reference the actual rule against Medicare.gov or your state's Medicaid agency. If you're using AI this way, our piece on how to verify medical information from AI tools is worth a read first.

What AI Can't Do in Medicare and Medicaid Navigation

As useful as these tools are, there are categories of decisions where AI has real limits, and the wrong tool can cost a family money or time they can't get back. Here are the situations where families need to bring in a human professional, and where stopping at the AI answer can produce real damage.

Replace a Medicaid Planning Attorney

Asset protection, look-back period strategies, irrevocable trusts, and spend-down planning involve state-specific rules and a five-year federal look-back window for Medicaid eligibility on long-term care. Mistakes here are expensive and often irreversible. An elder law attorney with Medicaid expertise is the right professional for this work. AI can summarize what these strategies are, but it can't safely execute them, and the cost of a wrong move on a Medicaid asset transfer can wipe out years of carefully accumulated savings.

Replace a SHIP Counselor or Independent Broker

For complex plan selection (multiple chronic conditions, specific provider networks, expensive medications, dual-eligible situations), the right human is a SHIP counselor or a licensed independent broker who isn't captive to one carrier. They know the local market and which plan denied which claim last year, and that institutional memory is something no AI tool currently has access to.

Win a Medical Necessity Appeal

AI can scaffold an appeal letter, but it can't replace the physician statement that wins a medical necessity dispute. The tools also can't predict your state's specific Medicaid waiver wait times, which vary dramatically and depend on local funding cycles, current waitlist positions, and case-specific priority criteria that aren't visible in publicly available data anywhere on the open web.

Replace a Hospital Discharge Planner

When an elderly parent is being discharged from a hospital, the social worker doing discharge planning has more practical pull than any AI tool will. They know which skilled nursing facilities currently have beds, which ones accept Medicare versus Medicaid, and which ones to avoid based on what they've seen come back to the ER. I see this work happen from the radiology side every week, and the discharge planner is one of the most underused resources families have access to.

What a Family Might Actually Do

Here's the recommended sequence when you're staring at the volume of decisions in front of you. It works whether your parent is newly diagnosed or already deeper into a care transition, and the order matters more than most families realize.

1. Start at the Neutral Baseline

Open Medicare.gov Plan Finder and NCOA BenefitsCheckUp, and run your parent's situation through both before doing anything else. Print or save the results, because this gives you a neutral, government-or-nonprofit baseline before you talk to anyone with a sales incentive. The information you collect here will surface questions you didn't know to ask, and those questions are what make the next conversation productive.

2. Schedule a SHIP Consultation

SHIP counseling is free, state-operated, and doesn't sell anything, and most appointments are scheduled within one to two weeks. Bring the printouts from step one. The counselor will catch things the tools missed and explain how local plan networks actually work in your parent's area, which is often where the real differences between plans show up.

3. Consult an Elder Law Attorney for Medicaid Planning

If long-term care is on the horizon and Medicaid eligibility might matter, talk to an elder law attorney with Medicaid expertise, because the five-year look-back rule means timing matters. Many attorneys offer reduced-fee initial consultations through the National Academy of Elder Law Attorneys. Our piece on Medicaid planning basics for memory care covers the foundation before you walk into that consultation.

4. Use AI as Scaffolding, Not Authority

Throughout the process, ChatGPT or Claude can help you draft questions, summarize letters, organize information, and make sense of denial codes, and you should use them this way. Don't treat their answers as final on rule-specific questions, and cross-reference against the actual source. The verification habits matter more than which tool you choose.

The Bottom Line on AI Tools for Medicare and Medicaid Navigation

AI tools have made parts of Medicare and Medicaid research faster and clearer for families, but the basic truth hasn't changed: the work of getting your parent's coverage right still depends on human judgment at the points where it matters, including a SHIP counselor for plan selection, an elder law attorney for Medicaid planning, and a hospital social worker for discharge transitions. The right AI tool helps you arrive at those conversations more prepared, while the wrong AI tool wastes your time and your privacy. If a tool asks for your phone number before showing results, close the tab. If recommendations don't change when the inputs change, the math isn't real. Stick with Medicare.gov, BenefitsCheckUp, your state's SHIP program, and verified general AI for scaffolding. That combination, used carefully, is more than enough to get you and your parent through this stretch with the coverage you actually need. You've got this.