Picture this: your mother is 78 years old. Her husband, your father, was a Korean War veteran who passed away a few years ago. She's been living alone since, but in the last eight months something has shifted. She's forgetting appointments. She called you twice last week asking the same question. Her doctor used the word "dementia" for the first time. Now your family is looking at memory care costs of $7,000 or more per month, and you're trying to figure out what VA survivor benefits she might qualify for to help pay for it.

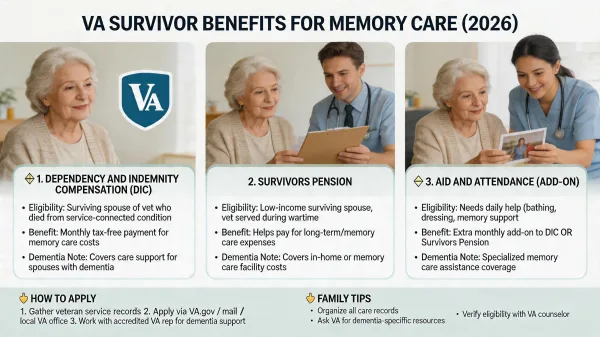

This is the situation a lot of adult children find themselves in, and the answers aren't as clear as they should be. The VA offers three different benefits that can help surviving spouses of veterans pay for memory care: Dependency and Indemnity Compensation (DIC), Survivors Pension, and Aid and Attendance added to either of those. Each has different eligibility rules. Each pays a different amount. And the VA won't pay both DIC and Survivors Pension at the same time, so understanding which one your parent qualifies for, and which pays more, matters.

I lost my first husband at 27, and I know what it's like to face paperwork while grieving. VA survivor benefits are not something I've personally claimed, but I've done substantial research to put this article together, and I've sat with families who were trying to read VA forms through the fog of loss. These benefits are complicated, and this article is my attempt to make them less so.

The Three Main VA Survivor Benefits for Memory Care

Before getting into the details, here's how the three benefits compare at a glance. This table is based on 2026 rates, which took effect December 1, 2025.

| Benefit | Based On | 2026 Monthly Max (surviving spouse, no dependents) | Income-Tested? |

|---|---|---|---|

| DIC (Dependency and Indemnity Compensation) | Service-connected death or totally disabled veteran | $1,699.36 base + add-ons | No |

| Survivors Pension | Wartime service plus financial need | $974/month base (no A&A) | Yes |

| Survivor A&A (Aid and Attendance) | Need for help with daily activities, added to DIC or Pension | Adds $421/month to DIC; raises Pension max to $1,558/month | Depends on base benefit |

Survivor A&A isn't a separate benefit. It's an add-on that increases either DIC or Survivors Pension when the surviving spouse needs regular assistance with daily activities or is in a care facility for physical or mental incapacity. Dementia qualifies, which is the piece most families don't realize.

DIC, Survivors Pension, and Survivor A&A: How They Differ and Who Qualifies

The three benefits are built on different foundations, and understanding those foundations is the key to figuring out what your parent qualifies for.

Dependency and Indemnity Compensation (DIC)

DIC is a tax-free monthly payment for surviving spouses, children, and in some cases parents of veterans whose death was caused by military service or a service-connected condition. It's not income-tested. A surviving spouse qualifies for DIC if the veteran died from a service-connected injury or illness, or if the veteran was rated totally disabled by the VA (including total disability from individual unemployability) for at least ten years before death, or for at least five years if the rating started at separation from service. There's also an eight-year provision that adds $360.85 per month if the veteran was totally disabled for the eight full years before death and the spouse was married to the veteran during that entire period.

The surviving spouse also has to meet marriage rules: married to the veteran for at least one year before death (or less if a child was born of the marriage), lived continuously with the veteran until death, and not remarried (though remarriage after age 57 doesn't end the benefit). The 2026 base monthly rate is $1,699.36 effective December 1, 2025, and that's before any add-ons.

Survivors Pension

Survivors Pension, sometimes called Death Pension, is a needs-based benefit for low-income un-remarried surviving spouses of wartime veterans. Unlike DIC, the veteran's death doesn't have to be service-connected. What matters is wartime service and the surviving spouse's current financial picture. The VA recognizes specific wartime periods: World War II (December 7, 1941 to December 31, 1946), Korean conflict (June 27, 1950 to January 31, 1955), Vietnam era (February 28, 1961 or August 5, 1964 to May 7, 1975 depending on where the veteran served), and Gulf War (August 2, 1990 through a future date set by Congress).

The veteran needs to have served at least 90 days of active duty with at least one day during a covered wartime period if they entered active duty on or before September 7, 1980, or 24 months for those who entered later. The discharge also can't be dishonorable. On the surviving spouse side, Survivors Pension is income-tested and net-worth-tested. The 2026 net worth limit is $163,699, and that includes most assets plus annual income (the primary home, car, and basic household items don't count). There's also a three-year look-back on asset transfers, so moving money out of a parent's name right before applying can trigger a penalty period of up to five years.

Survivor Aid and Attendance

Survivor A&A isn't a standalone benefit. It gets added to DIC or Survivors Pension when the surviving spouse needs regular help with activities of daily living, is bedridden, has severely limited vision, or is a resident of a care facility because of physical or mental incapacity. Dementia falls squarely in that last category once cognitive decline is documented and care needs are established. Added to DIC, A&A brings an extra $421 per month in 2026. Added to Survivors Pension, A&A raises the Maximum Annual Pension Rate (MAPR) ceiling to $18,697 for a surviving spouse with no dependents, or about $1,558 per month at the maximum.

Can DIC and Survivors Pension be combined?

No. If a surviving spouse qualifies for both, the VA pays whichever produces the larger monthly amount. Most families discover that DIC pays more when eligibility exists, which is why confirming service-connection status matters so much before filing.

How Much These Benefits Pay in 2026

The 2026 numbers matter because they set the realistic expectation for how much of a memory care bill these benefits can cover. A surviving spouse with no dependents who qualifies for DIC receives $1,699.36 per month as the base rate. Add the eight-year provision and A&A, and that figure climbs to roughly $2,481.21 per month. The eight-year provision only applies in specific circumstances, but A&A is commonly approved for surviving spouses in memory care.

For Survivors Pension, the calculation works differently. The VA subtracts the surviving spouse's countable income from the applicable MAPR, and what's left is paid out in twelve equal monthly installments. A widow with $14,000 in annual Social Security income who qualifies for Survivors Pension with A&A (MAPR of $18,697 in 2026) would receive about $4,697 per year, or roughly $391 per month. But unreimbursed medical expenses above 5% of the MAPR (about $935 for a surviving spouse with no dependents) reduce countable income, which can raise the monthly payment substantially. Memory care costs paid out of pocket generally qualify as unreimbursed medical expenses.

That math adds up fast. A widow whose only income is Social Security, who's paying $7,500 a month for memory care, may end up with zero countable income after medical expense deductions and receive close to the full $1,558 per month of A&A-enhanced Survivors Pension.

Using VA Survivor Benefits to Pay for Memory Care

Once approved, DIC and Survivors Pension payments arrive as tax-free monthly deposits the surviving spouse can spend however care needs require. The VA doesn't restrict how the money is used. It can go toward memory care community fees, in-home care, adult day programs, or any other care-related expense. The median monthly cost of memory care in the United States ranges from roughly $7,000 to $8,500 depending on the data source and region, with annual costs easily crossing $90,000. VA benefits rarely cover the full bill on their own, but they can close a meaningful gap when combined with Social Security, pension income, savings, and family contributions.

Families often discover that the monthly cost they were quoted doesn't include medication management, incontinence care, or higher levels of supervision that dementia residents usually need as the disease progresses. Planning for VA benefits alongside other funding sources gives the household a longer runway before savings run out. Starting early matters. Applications can take months to process, and retroactive benefits only go back to the filing date.

Where Families Get Stuck

Most Survivors Pension denials and delays come from the same handful of issues, and knowing them ahead of time saves families months. The first is missing or incomplete proof of the veteran's wartime service. A DD-214 (discharge paperwork) is the document the VA wants, and without it, the application can stall while the National Personnel Records Center searches for a copy. If you can't find the veteran's DD-214, you can request a replacement using Standard Form 180 through the National Archives.

The second common problem is incomplete financial disclosure for Survivors Pension claims. The VA wants a full picture of assets, income, and any transfers within the three years before the filing date. Leaving out a life insurance cash value, a brokerage account, a small rental property, or a recent gift to an adult child can trigger a deeper review or a penalty period, and the look-back rule applies even if the transfer was made for entirely benign reasons like estate planning. Third, A&A applications fail when the medical documentation is thin. A single note that says "patient has dementia" isn't enough. The VA wants specifics: what activities of daily living does the person need help with, how often, and for how long is the need expected to continue. A physician's completed VA Form 21-2680 (Examination for Housebound Status or Permanent Need for Regular Aid and Attendance) addresses this directly, and most primary care doctors will complete it if asked.

Applying as a Surviving Spouse With Dementia

This is where a lot of families run into a problem they didn't see coming. A surviving spouse with early-stage dementia may still be able to sign her own application, but as the disease progresses, the question of who can legally act on her behalf becomes central. Families often assume that an existing durable power of attorney solves the problem. With VA benefits specifically, it doesn't.

The VA runs its own program called the Fiduciary Program. When the VA determines that a beneficiary cannot manage her VA benefits because of injury, disease, or age (dementia clearly qualifies), the VA appoints a fiduciary to receive and manage those payments on her behalf. A durable power of attorney executed outside the VA system has no automatic standing in the fiduciary process. The VA conducts its own field examination and makes its own appointment, and while the VA considers the beneficiary's preference first (usually a spouse or adult child), the appointment isn't guaranteed to go to the person named in the power of attorney.

This experience has shown me how surprised families are when they're told the power of attorney they paid an attorney to prepare doesn't automatically extend to the VA. A family member's dementia moved faster than any of us expected, and decisions we thought we had time to make ended up needing to happen under pressure, with the grief of losing who that person used to be sitting underneath every conversation. I mention this because the same pattern plays out with VA benefits. Families assume the legal paperwork they already have is enough. With the VA, it usually isn't. The Fiduciary Program is its own process, and starting it earlier rather than later makes everything else easier. The person the VA ultimately appoints as fiduciary goes through a background check, a credit review, and an interview, and that takes weeks. The delay hurts most when a family is also trying to move a parent into memory care and keep monthly bills current.

Practically, this means an adult child who expects to manage a parent's VA benefits should plan to submit a Potential Fiduciary Application through the VA's Access VA portal as soon as the benefits application is filed, not after. If no family member is available, the VA can appoint a professional fiduciary, who is allowed to charge up to 4% of the monthly benefits as a fee. That fee comes directly out of the surviving spouse's payments, so keeping the appointment within the family protects the monthly benefit amount.

One practical note: the VA fiduciary only has authority over VA benefits. It doesn't affect Social Security, private pensions, bank accounts, or any other assets. Those still require the ordinary power of attorney and, in some cases, a separate representative payee for Social Security.

Documentation You'll Need Before Filing

Gathering paperwork before sitting down to fill out VA Form 21P-534EZ (the combined application for DIC, Survivors Pension, and Accrued Benefits) saves weeks on the back end. At minimum, you'll want the veteran's DD-214 or other separation documents, the veteran's death certificate, the marriage certificate showing the date of marriage, divorce decrees from any prior marriages for either spouse, and a complete list of the surviving spouse's income and assets.

If applying for A&A, also gather medical records documenting the dementia diagnosis, a physician's statement on VA Form 21-2680, and records of any ongoing care. If the surviving spouse is already in memory care, include the facility's admission paperwork and monthly invoices. The invoices serve double duty: they prove the need for aid and attendance, and they document unreimbursed medical expenses that reduce countable income for Survivors Pension calculations.

Common Questions Families Ask

Does a widow have to reapply for DIC each year? No. Once approved, DIC continues automatically, with annual cost-of-living adjustments applied. Survivors Pension does require annual income verification through an Eligibility Verification Report.

What happens if the widow remarries? Remarriage generally ends DIC and Survivors Pension, with an important exception for DIC: remarriage after age 57 does not end DIC. For Survivors Pension, any remarriage ends eligibility.

Can benefits be backdated? The effective date is usually the date the VA receives the claim. In some cases, an intent-to-file submitted first can preserve an earlier effective date for up to a year while the full application is prepared.

Do VA survivor benefits affect Medicaid? They can. In most states, the basic Survivors Pension amount counts toward Medicaid income limits, while the A&A portion is usually exempt. Rules vary by state, and anyone considering both Medicaid and VA benefits should talk with an elder law attorney or Medicaid planner familiar with the dual-eligibility rules.

Is there a cost to apply? No. The application itself is free, and working with a VA-accredited VSO representative is also free. Anyone charging a fee to help file an initial VA claim is violating federal law.

What to Do Next

VA survivor benefits won't erase the cost of memory care, but for an eligible widow or widower they can cover a real portion of it, month after month, tax-free. The hardest part for most families is the beginning: sorting out which benefit applies, gathering the documentation, and understanding that the VA has its own rules about who can act on behalf of a surviving spouse with dementia. None of this has to happen all at once. Starting with the benefit that's most likely to apply, usually DIC if the veteran had a service-connected condition or Survivors Pension if the veteran served during wartime and the household has limited income, moves things forward.

If you're reading this with your own mother or father in mind, give yourself permission to take it one step at a time. Gathering the veteran's DD-214 is a step. Calling an accredited VSO is a step. Requesting the VA Form 21-2680 from the primary care doctor is a step. Each one gets you closer to an answer, and answers are what families need most right now.